Mortgage Lenders Most Asked Questions Answered

Lenders need to keep up with the latest trends to gain a competitive edge. We compiled our most frequently asked questions from Mortgage lenders and laid them out for you below. The lending FAQs can help you expand access to credit and improve the mortgage experience for homebuyers.

Why should I use a mortgage credit report with telco, pay tv and utilities insights?

The current mortgage tri-merge credit report combines reports from all three bureaus into a single document. This provides a more comprehensive picture of an applicant’s credit history. Equifax is now making telco, pay tv and utilities insights available to be delivered alongside tri-merge credit reports. This now allows lenders to receive 15 new telco, pay tv and utilities attributes directly reported by 160+ telco, pay tv and utilities contributors, so lenders can see a better view of historical payment and credit behaviors

For example, Home ownership continues to be a primary contributor to successful wealth building, yet there are strong barriers to home ownership for credit invisible consumers across the mortgage financial system. Borrowers with thin or unscorable credit files can be locked out of qualifying for a loan,or left to a manual-paper based process, because the entirety of their financial profile is not being considered. Access to this additional differentiated data provided lenders with insights on 191 million unique consumers - exclusively from Equifax.

These provide powerful new insights that help to automate, save time and resources, and streamline the first mortgage process for every applicant – creating more potential for millions of Americans to achieve their goal of homeownership.

How can supplemental reports help me and my customers?

A lot can happen between loan application and closing. Supplemental reports can help provide verified updates to a homebuyer’s file during the underwriting process. Supplements are typically requested when information within the credit report requires additional information or updates in order to meet the lender’s and/or Government Sponsored Enterprises (GSE) underwriting requirements, such as:

Confirming Derogatory items

Update to payment history

Updated balances since the loan application was initiated

And more

You can identify opportunities to help an applicant improve their chances of qualifying or getting a better rate, while taking a consultative approach to improving the lending experience. Here are just a few solutions available through Equifax:

Edited Credit Hi Lite (ECHL) Supplemental report — Let’s say a consumer notices that the balance on their credit card reporting on the tri-merge credit file is higher than it is today as they just paid down their credit card a couple of days prior. Our ECHL process allows the lender to obtain the updated balance. The lender can then include it in the consumer debt to income ratio evaluation instead of waiting for the creditor to update the credit bureaus. This service can also add rental history that can be used in underwriting as well.

Accelerated Rescore — In the case of disputed or incorrect credit information, this service can update tradelines with the credit reporting agencies in less then 48-72 hours.

Credit Xpert® What If Simulator™ — The “what if” simulator estimates how a change in behavior can impact a client’s credit. This can lead to improved credit scores, better terms, increased sales volume, and better customer experiences.

Credit Xpert® Wayfinder™ — When a low-scoring customer has the potential to improve, Wayfinder helps generate a personalized plan that provides specific steps they can take to attain the score they need.

Credit Xpert® Credit Assure™ — This report includes not only the credit score, but also the applicant’s score potential, so you can judge their potential to qualify for a loan or a better loan program. When used with an Accelerated Rescore, it can help them obtain the best rates possible, based on their credit.

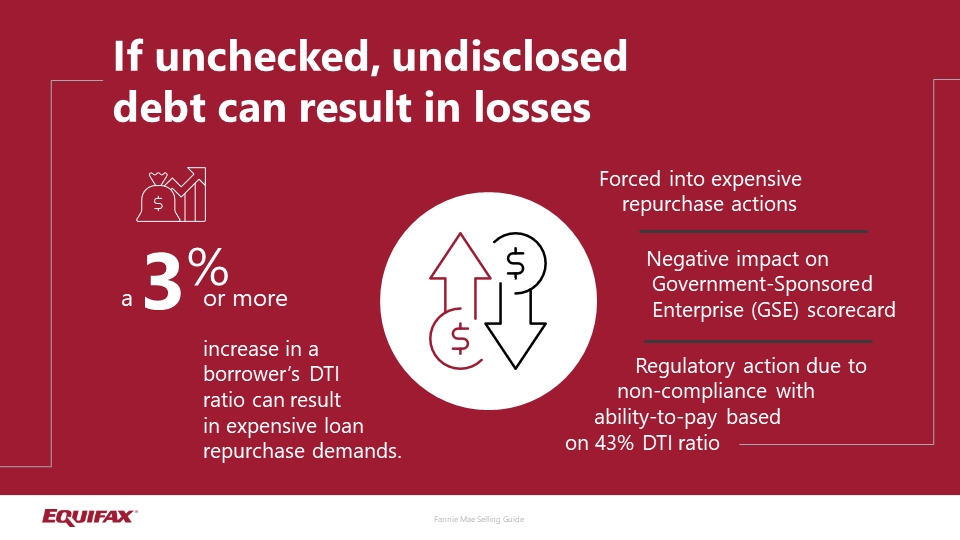

Why should I care about undisclosed debt monitoring?

Undisclosed debt is any liability that exists at the time of closing that the borrower doesn’t disclose during origination. This can include auto leases, loans, mortgages, revolving credit, or installment loans.

The GSE guidelines require lenders to look into undisclosed debt as part of its underwriting requirements. This can be difficult, as many homebuyers incur new debt after the initial mortgage application before closing. This can result in an increase in potential risk. In fact, 36% of borrowers who opened a single new tradeline before closing increased their debt-to-income ratio by at least 3%.1

How can undisclosed debt impact a mortgage loan?

Undisclosed debt can disrupt mortgage closings, overload underwriting resources, and ruin the customer experience. When a borrower doesn’t disclose all obligations — both new and existing — the calculated debt to-income (DTI) ratio is inaccurate. That means the mortgage lender can’t accurately evaluate a borrower’s ability to repay. It can also keep borrowers from qualifying for favorable rates, and potentially lead to a rejected application.

By stressing the importance of avoiding new debt, you can help borrowers close more easily. Also, borrowers can secure the best possible terms based on their records, and enjoy a more positive experience. More visibility into borrower activity may reveal misrepresentation or undisclosed debt. By using a debt monitoring solution, lenders can better mitigate risk and streamline underwriting efforts.

How can I better inform my customers about mortgages, loans, and credit scores?

Equifax has the technology mortgage lenders need to make smarter decisions and help homebuyers achieve the dream of homeownership. Read our blog, "Help Borrowers Move Through the Mortgage Process" for more insights and how you can help your potential borrowers or visit our consumer knowledge center for resources to help your borrowers. For more information, visit Equifax.com/business/mortgage

[sources]

1 From Equifax analysis based on an anonymous sample of 105,000 mortgage applicants

Recommended for you